April 17, 2017

Cartier Resources Inc. (TSX-V: ECR): Discovery in the Prolific Abitibi Gold Belt in Quebec, Sponsored by Agnico Eagle: Interview with Philippe Cloutier, President and CEO By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA on 4/11/2017

Cartier Resources Inc. (TSX-V: ECR): Discovery in the Prolific Abitibi Gold Belt in Quebec, Sponsored by Agnico Eagle: Interview with Philippe Cloutier, President and CEO

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 4/11/2017

Cartier Resources Inc. (TSX-V: ECR) is an exploration company focused exclusively on discovery in the prolific Abitibi Gold Belt in Quebec. We learned from Philippe Cloutier, who is president and CEO of Cartier Resources, that around 2011-2012 they adopted a new corporate strategy that was to identify and acquire projects of merit that had historic resource estimates, or ounces in the ground. Today in early 2017, they have attracted the sponsorship of a major mining company Agnico Eagle, who invested $4.5 million in December of 2016 to own just under 20%. Currently, the company launched a 50-thousand-meter drilling program targeted directly beneath the established showings and high-grade resources on four projects: their flagship Chimo Mine project, the Benoit project, the Wilson project, and the Fenton project. With nine million dollars in the bank, an experienced team and proven exploration strategy, Cartier Resources is ready to conduct a very dynamic and aggressive exploration program on some really high profile projects.

Dr. Allen Alper: This is Dr. Allen Alper, Editor-in-Chief of Metals News, interviewing Philippe Cloutier, who is president and CEO of Cartier Resources. Could you give our readers an update and an overview of your company?

Philippe Cloutier: Cartier Resources was listed ten years ago. From 2007 up until the most recent start of the crisis, which was late 2011-2012, we were progressing well and focusing on grassroots exploration. When the markets turned brutally in 2012, crashed and stayed really low for the ensuing four years, Cartier had about $4 million in the bank. Essentially we decided to upgrade our product, and we redesigned our corporate strategy. The basis of the corporate strategy was to identify and acquire projects of merit that had historic resource estimates, or ounces in the ground. Again, we focused exclusively in the Abitibi greenstone belt.

Today in early 2017, the outcome of that four-year shopping spree to acquire deposits, attracted the sponsorship of a major mining company, Agnico Eagle, who invested $4.5 million in December of 2016 to own just under 20%. They have an ownership of 19.9% of our shares. We have a great technical relationship with them as we can always count on them for expert technical advice.

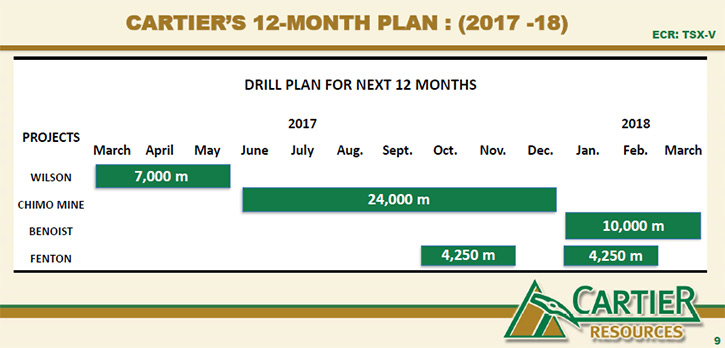

The market was so impressed, more investors wanted in, and we added another $3.5 million to the till. Today, at the end of March 2017, we sit with just under $9 million in the bank. We’ve launched a fifty thousand meter diamond drill program that’s going to cost us roughly about $5 million. Even at the end of this aggressive exploration diamond drill program, we will be left with a sizeable amount in our treasury.

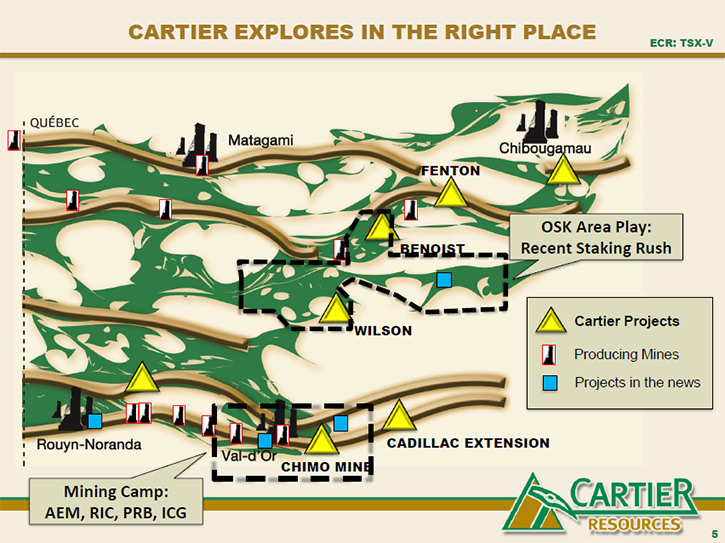

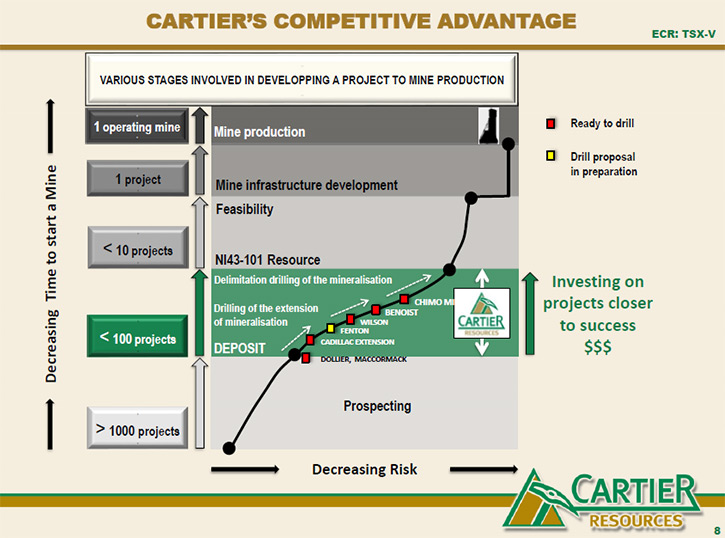

The fifty thousand meter diamond-drill program will be directed at drilling directly beneath the established showings and resources on four projects, the flagship being the Chimo Mine Project. Then we have the Benoist project, and then Wilson, and then finally Fenton. In a nutshell, that’s how we’ve progressed from listing in 2007 to where we are today in 2017. As a junior company we have a very robust treasury and we are going to focus diamond-drilling directly on the extension of known high-grade gold mineralization in the Abitibi.

Dr. Allen Alper: That sounds great. I’m very impressed with what you’ve done in the last few years. That’s excellent.

Philippe Cloutier: I could describe the individual assets, if you wish.

Dr. Allen Alper: Yes, excellent.

Philippe Cloutier: All of the technical information is presented on our website, www.ressourcescartier.com.

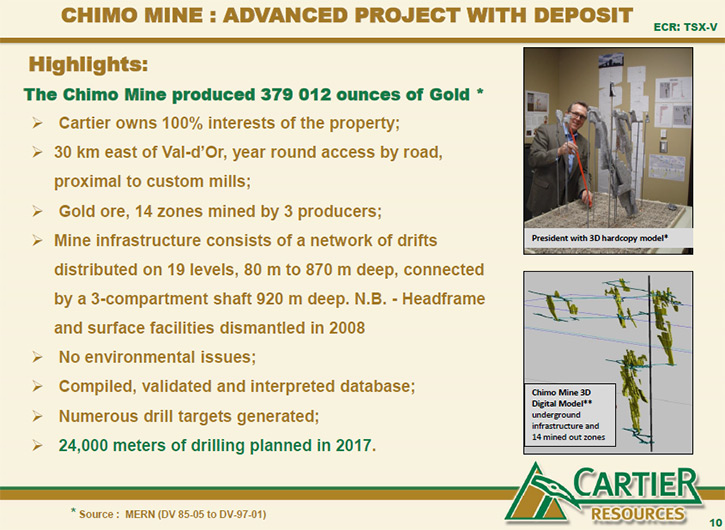

Let me start with the Chimo Mine project, a past producer. It actually produced three times, once in the 1960s, a smallish amount of gold ounces on a northern shear, where it had relatively high-grade thin veins. In the mid-eighties another company picked it up. They mined just under a hundred thousand ounces on the extensions of the previous mine, but they found some new stuff slightly to the south and they initiated mining there. They sold that project to Cambior Mines. Cambior then extracted, at depth, an extra two hundred twenty thousand ounces of gold. In total about four hundred thousand ounces of gold were taken from the same vein systems.

When Cambior threw in the towel in 1997, it wasn’t for lack of ore. It was because the price of gold at that time was $275 USD an ounce, too low to be profitable to continue mining. Also, Cambior had their own issues with other deposits, and they were going through some corporate struggles, and so they not only shut the Chimo Mine down, but also two other deposits in the Abitibi, a reflection of their corporate situation and the weak gold price. Then the project was shelved. It was picked up by a company called Blue Note Mining, who never worked the project. Instead they tried mining zinc in New Brunswick, and ended up going bankrupt.

Cartier was present in 2013, and bought the deposit for $261,000. Today the surface infrastructure has been taken out, but the shaft is preserved with a concrete collar plate, and was flooded. It goes down to 920 meters vertical. Previous mining had only gone down to 870 meters. In the last few years we’ve assembled a comprehensive database, including about four thousand diamond drill holes, and sixty thousand assays. Agnico was quite impressed by the project and decided to become a strategic partner with Cartier by owning the shares.

You can find a detailed description of the mineralization, and all the technical data, on our website. It’s our flagship. Starting late May or early June we will bring in one machine and a second the month after that. We’re targeting twenty four thousand meters of diamond drilling on the project. One machine will be directed at drilling very deep below the main mine vein set that produced most of the ounces. The other drill machine will be drilling economic targets in the lateral extensions of the main vein set and the prospective northern shear. The hope is to scope out sufficient ounces of gold that would prompt a senior mining company, if not Agnico themselves, to take over the project from there and bring it into production. Obviously that would be to the benefit of the Cartier shareholders.

Dr. Allen Alper: That’s excellent. That’s really impressive.

Philippe Cloutier: It is, because one of the technical merits of the project is that it sits right by the highway, about a thirty minute drive from downtown Val-d’Or. It has infrastructure that goes right up to the previous mine site, in terms of power lines, and access roads. It has access to a very qualified workforce. It is in an area that is steeped with mining culture and acceptance. Any success we have on the project will be rewarded by local acceptance and fast tracking of any future development if warranted. That also adds a lot of value to the project, and is an instant reward element for our investors and our shareholders.

Dr. Allen Alper: That’s excellent. Could you tell our readers and investors about yourself, your background?

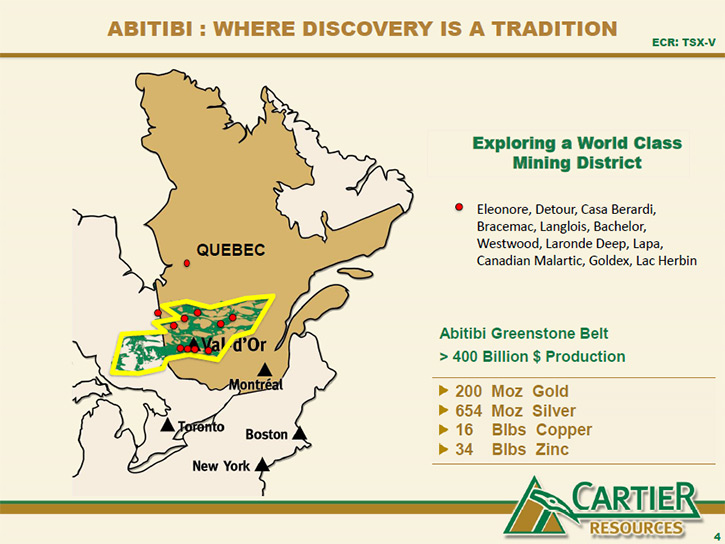

Philippe Cloutier: Yeah. I’m a geologist. I graduated in 1986, with a Bachelor of Science in Geology from the University of Montreal. My career developed over twenty years. I worked for firms like Aur Resources, Noranda, SOQUEM, some junior exploration companies, and some consulting firms. My career path brought me to look at projects all over North America, including Southwest US, Central America and Mexico. I would always come back to the Quebec Abitibi Greenstone Belt because all the political risk, all the environmental risk, all the financing risks are minimal in the Abitibi. It’s an area where there have been hundreds of mines in the past hundred years, and especially access to tremendous workforce and infrastructure.

As a geologist, I’m very cognizant of the fact that exploration is high risk. It’s a high risk industry, and you have to de-risk as much as possible; be it a cultural risk, a political risk, a financial risk, and even an endowment risk. The Abitibi’s endowment in terms of gold and base metals is well known. It’s a place where discovery is a tradition, and people can be rewarded very rapidly for their discoveries.

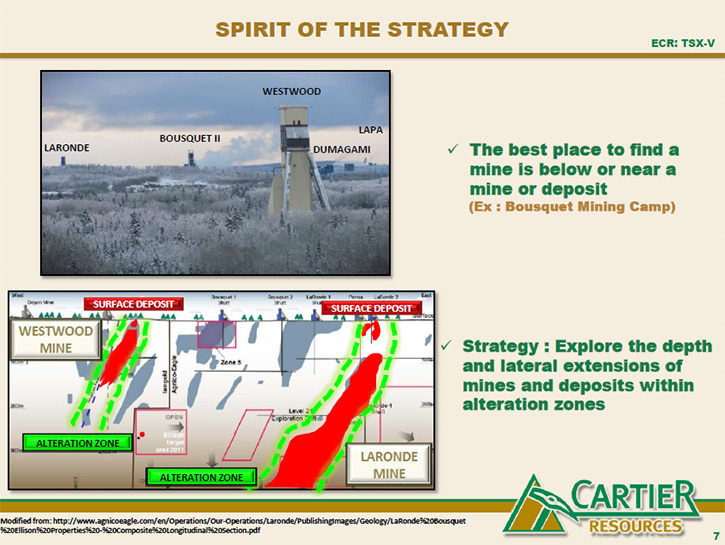

From 2003 to 2016 there were many projects that were drilled, permitted, and brought into production, and these include things like Lac Herbin, Goldex, Lapa, Canadian Malartic, Laronde, Westwood Deep, Detour, Bachelor Mine, so many of them. Small mines, high grades with small tonnages, large tonnages with low grades, some were developed by junior companies, some were developed by senior companies. The common denominator was that none of the deposits or mines were new discoveries. They were all old exploration or mining plays that had been shelved for different reasons, such as bad economic conditions, corporate strategic reasons, companies leaving the area, but none of these that were brought into production very recently were actually new discoveries. They were projects that had known their glory days in the early or late eighties and nineties, and then just shelved for a whole bunch of reasons that did not match their potential.

That’s what we call renaissance exploration. You go back to old districts, where the endowment is clearly there, and with new economic conditions or new innovative or technological developments, mineralization then becomes ore. With the right price of metals you could reboot a project and get it up and running again. As a geologist, as a financier and an entrepreneur, I think it makes a lot of sense to explore and focus in the Abitibi. Obviously companies like Agnico Eagle believe that as well, so they continue to mine and explore in the Abitibi. They’ve also decided to invest in companies that also believe in the Abitibi. So we were rewarded last December with a significant sponsorship from them.

That puts us in a situation where today we have just under nine million dollars in the bank, more than enough to conduct a very dynamic and aggressive exploration program on some really high profile projects.

Dr. Allen Alper: That sounds excellent. Could you tell our readers/investors a little bit more about your share structure, where your shares are listed?

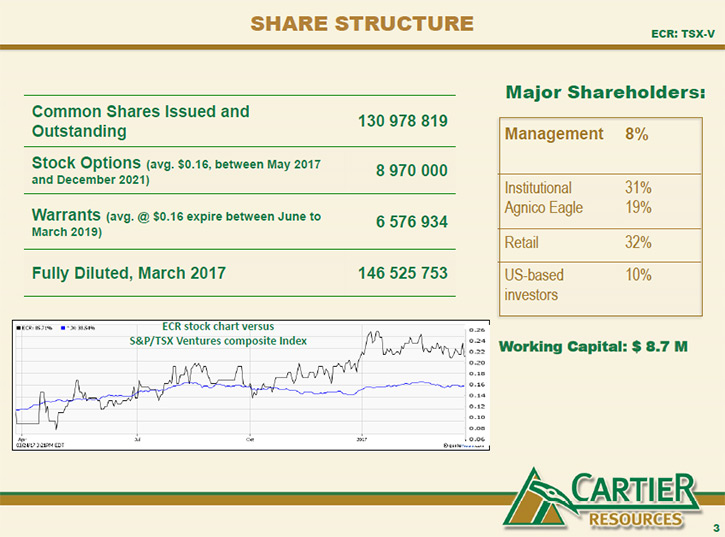

Philippe Cloutier: Indeed. We currently have just over 130 million shares outstanding. That may sound a bit on the steep side. But in the past five or six years, as we kept printing shares for money to weather our storm, the shares were actually going to previous shareholders, so we’re looking at a company that’s more like a private investment club, rather than a publicly traded company. We have a very tight share structure, a very few core long-term and loyal shareholders that believe in our business model and are waiting for better times to translate that into a proper valuation for Cartier.

It’s very difficult to acquire a sizeable position in Cartier because our current shareholders aren’t willing to part with their shares very easily. It’s a reflection of the fact that we have people or supporters that believe in our story, and that also believe that this next bull market is going to finally reward them.

I encourage people to take a look at our company, our technical merits and assets, and to make a decision whether you want to patiently accumulate our stock.

Dr. Allen Alper: That sounds great. What are the primary reasons our high-net-worth readers/investors should consider investing in your company?

Philippe Cloutier: We’re a company with a very solid management that, a few years ago, decided to invest in an area of the world that is known to reward investors. We focus exclusively in the Abitibi Greenstone Belt. We focus exclusively on projects of merit, the higher end, more advanced exploration plays that already have historical gold estimates, and add value.

We also have been able to get the large mining companies to vouch for our process, vouch for our expertise, and vouch for the quality of assets that we have brought in. I think investors will understand a company such as Agnico Eagle probably hasn’t bought into us at the $0.20 level to flip those shares over at $0.25. I think they’re in for the long run to see what we can do at Chimo, Benoist, Fenton, and Wilson.

I think if sophisticated investors want to invest their money, while minimizing the risk generally associated with the exploration process, they should take a hard look at what we’re doing. Their money would be invested directly in the ground. Greater than 85% of the monies invested this year will be in direct diamond drilling of known mineralization. We’re drilling directly beneath and along strike and mineralization that is of economic merit. I think we’re a low cost, low risk, and high reward situation, especially in light of the market turnaround.

Dr. Allen Alper: Those sound like excellent reasons why our high-net-worth readers/investors should consider investing in Cartier Resources.

http://www.ressourcescartier.com/

Philippe Cloutier, P.Geo.

President and CEO Telephone: 819 856-0512

philippe.Cloutierer@ressourcescartier.com